Monthly Market Update

Submitted by TLWM Financial on July 1st, 2022

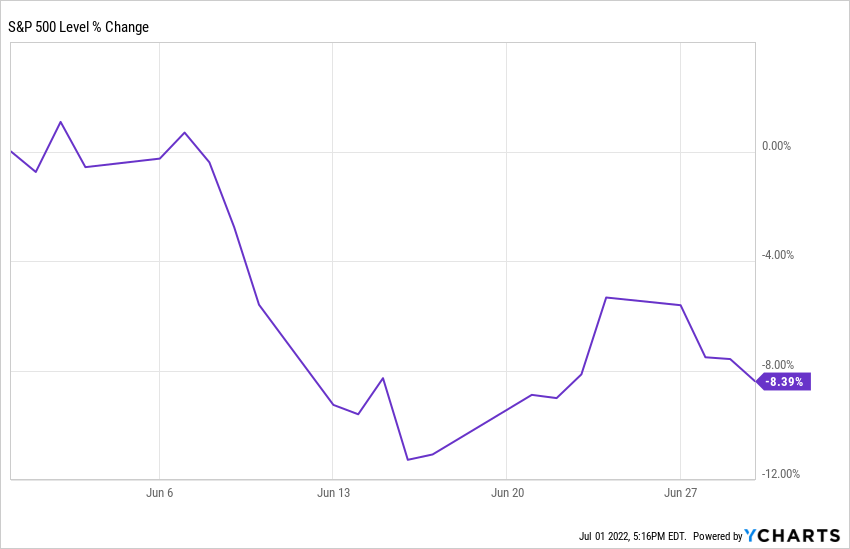

The challenging first half of 2022 is now in the books as the S&P 500 dropped roughly 8% in June bringing the year-to-date return to about -20.5%. While stocks struggled, they were not alone, as most asset classes have been negatively impacted this year, including fixed income, with the US Aggregate bond market down about 11% for the year.

The good news is that we made changes to portfolios in April to manage risk due to the fact that we felt the chances of recession were rising. Thus far, that change has been a good one for portfolios and we continue to have a portion of our growth portfolios defensively positioned today.

Now, most investors are concerned about what may come next. With that in mind, we’d like to invite you to our upcoming mid-year outlook breakfast on July 16th. Click here to RSVP and please feel free to invite any friends, family, or colleagues that you think would be interested in hearing more about what we feel is to come for the economy and market for the rest of 2022.

While we’ve had a variety of headlines throughout the year the main driver for the economy and the market has been inflation, the Federal Reserve’s response to inflation, and the risk it poses to economic growth moving forward. Thus far this year we’ve seen the Fed do the following:

- Raised rates in March by 0.25% - the first rate-hike since 2018.

- Raised rates in May by 0.50% and set expectations for more 0.50% hikes to follow.

- Announce and begin quantitative tightening – pulling liquidity out of the markets.

- Raised rates in June by 0.75%, the largest hike since 1994.

- Currently, expectations are for the equivalent of 13 total hikes of 0.25% in 2022. At the end of last year expectations were for only 3 hikes of 0.25%.

Clearly, the Fed has shifted monetary policy quickly in an effort to curb inflation. Policy changes tend to impact the economy with a bit of a lag so the question for most investors is whether a much more restrictive policy pushes the economy into a recession. If so, how deep will that recession be?

With that in mind, we will be watching economic data closely over the next couple of months to get a clearer sense of future Fed expectations along with the impact to the economy and our dashboard. As we outlined last month we are preparing for a variety of scenarios and will be ready to make adjustments to portfolios as needed. Those adjustments could see us reduce risk further or even put some cash back to work as we get a clearer picture of how the back half of 2022 is going to unfold.

We look forward to seeing you in-person at our Mid-Year Outlook event in July!

Sincerely,

Your Team at TLWM

* Investment advice offered through TLWM, LLC., a registered investment advisor.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged index. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

*Credit risk can be a factor in situations where an investment’s performance relies on a borrower’s repayment of borrowed funds. With credit risk, an investor can experience a loss or unfavorable performance if a borrower does not repay the borrowed funds as expected or required. Investment holdings that involve forms of indebtedness (i.e. borrowed funds) are subject to credit risk.

* Typically, the values of fixed-income securities change inversely with prevailing interest rates. Therefore, a fundamental risk of fixed-income securities is interest rate risk, which is the risk that their value will generally decline as prevailing interest rates rise, which may cause your account value to likewise decrease, and vice versa. How specific fixed income securities may react to changes in interest rates will depend on the specific characteristics of each security. Fixed-income securities are also subject to credit risk, prepayment risk, valuation risk, and liquidity risk. Credit risk is the chance that a bond issuer will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of a bond to decline.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Consult your financial professional before making any investment decision.

* Stock investing involves risk including loss of principal.

* This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where TLWM Financial and its representatives are properly licensed or exempt from licensure.

* No strategy ensures a profit or protects against a loss.