Weekly Market Commentary

Submitted by TLWM Financial on September 12th, 2016

The Markets

Blame it on the central banks!

After 44 consecutive sleepy, summer days when Barron’s reported the Standard & Poor’s 500 Index opened and closed without a 1 percent move in either direction, the index tumbled last week – and so did indices in other markets around the world. What roused investors from complacency? Some experts pointed their fingers at central banks:

“Three central banks announced their monetary policy decisions during the week and all three maintained the status quo and did not change policy. The news disappointed the markets – they were looking for more stimulus. And, in some cases, good economic data was interpreted as bad news because it meant that there was less of a probability of more stimulus.”

The U.S. Federal Open Market Committee doesn’t meet until September 20, but markets reacted sharply after Boston Fed President Eric Rosengren (whom Thomson Reuters labels as a dove) said, “My personal view, based on economic data that we have received to date, is that a reasonable case can be made for continuing to pursue a gradual normalization of monetary policy.” After his speech, Reuters reported the odds of a September Fed rate increase rose from 24 percent to 30 percent.

Expectations for market volatility moved higher, too, but markets weren’t too worried. The CBOE Volatility index (VIX) jumped 33 percent on Friday, reaching 16.56, according to MarketWatch. That was a big move, but significant market volatility is not indicated until the VIX moves above 20.

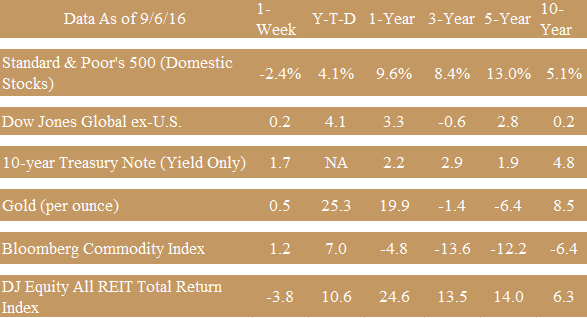

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; the DJ Equity All REIT Total Return Index does include reinvested dividends and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, Barron’s, djindexes.com, London Bullion Market Association. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

WHAT’S CHANGING IN WORLD MARKETS? GROCERY SHOPPING! Groceries may be mundane, but they’re big business. By 2020, the value of the world’s grocery market is expected to reach $11.8 trillion, according to The Institute of Grocery Distribution (IGD). The largest markets are expected to be China, United States, India, and Russia. That’s not the interesting part, though.

According to Morgan Stanley, fewer people will gather food by carting up and down the aisles of local grocery stores. Instead, in many countries, people will fill their baskets online. Globally, the share of shoppers buying groceries via the Worldwide Web and having them delivered is expected to grow from 21 percent in 2015 to 34 percent in 2016:

“Several factors may be driving the trend. Generally, more shoppers are accustomed to buying online, including a younger, more mobile generation of consumers. More specifically, boutique online-only grocery services in recent years have proven that the business model can work, overcoming logistical and consumer-behavioral barriers and building credibility for the category as a whole. Now, larger traditional players have entered the arena, offering more choices, services, and attractive prices, all within familiar eCommerce experiences and expectations for an even larger audience.”

Developed economies are expected to experience faster adoption rates. For instance, fewer than 10 percent of Americans bought fresh groceries online last year, but this year the percentage is expected to reach 26 percent. In Germany, just 10 percent of shoppers purchased groceries online. In 2016, that number is expected to rise to 36 percent.

In emerging markets, the expansion of online grocery shopping is dependent on the expansion of mobile networks. In countries like China and India, online grocers must leverage mobile networks to grow their market share.

Weekly Focus – Think About It

“People have been starting to focus less on the disability and more on the actual sport. I’ve had so many interviews that don’t even mention the backstory of how I became an amputee or whatever. I prefer that – I prefer being on the back pages with the rest of the sportsmen, not being just a heart-warming story.”

--Jonnie Peacock, British paralympic sprinter

Best regards,

Enzo T. Pellegrino CFP®

President & Wealth Advisor

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this e-mail with their e-mail address and we will ask for their permission to be added. Securities offered through LPL Financial, Member FINRA & SIPC. Investment Advice offered through Texas Legacy Wealth Management, a registered investment advisor and separate entity from LPL Financial.

* These views are those of Peak Advisor Alliance, and not the presenting Representative or the Representative’s Broker/Dealer, and should not be construed as investment advice.

* This newsletter was prepared by Peak Advisor Alliance. Peak Advisor Alliance is not affiliated with the named broker/dealer.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged index. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the afternoon gold price as reported by the London Bullion Market Association. The gold price is set twice daily by the London Gold Fixing Company at 10:30 and 15:00 and is expressed in U.S. dollars per fine troy ounce.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Consult your financial professional before making any investment decision.

* Stock investing involves risk including loss of principal.